The Bulls Still Control the Long-Term Trend

MULTIPLE TIMEFRAME ANALYSIS

Stocks: The Good, the Bad, and the Ugly

THE GOOD

A trend signal was triggered at the end of May that aligns with the thesis of a secular bull market driven by favorable demographics. As shown on the monthly chart of the S&P 500 below, the improvement in the stock market’s longer-term trend allowed the seven-month moving average to recapture the fourteen-month moving average. The signal was nailed down on May 31, 2023, with the S&P 500 trading at 4180.

The monthly signal above was triggered after the S&P 500 made a stand at an upward sloping 200-week moving average, which aligns with a secular uptrend.

Thus, it might be helpful to answer the following questions:

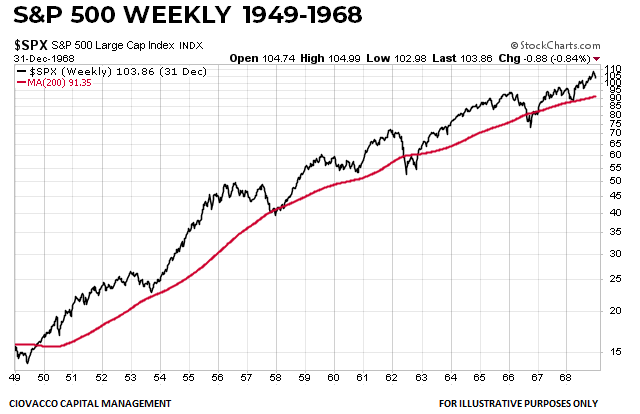

How many times was a similar bullish monthly moving average crossover signal generated in the context of the 1950-1968 and 1982-2000 secular bull markets?

How did the S&P 500 perform over the next year?

How large was the median drawdown over the next year?

Is the 2023 S&P 500 outside of the typical drawdown window?

Thus, our study period includes the window below that featured S&P 500 stands near an upward sloping 200-week moving average.

We also looked for bullish monthly moving average crossovers in the window below:

If we include the bullish cross following the major low in 1949, there were seven bullish crosses in the 1950-1968 window, including the 1954 case shown below.

There were five bullish crosses in the 1982-2000 window, including the 1988 case shown below.

The median and average S&P 500 returns following the twelve bullish monthly crosses that occurred within the context of a secular trend were very satisfying. The median one-year gain was 20.54%. The average one-year gain was 20.77%. The 2023 signal was triggered with the S&P 500 trading at 4180. Hypothetically, a 20% gain would mean the S&P 500 would be trading over 5,000 on May 31, 2024.

If the S&P 500 experienced an average or median maximum one-year drawdown, it would hypothetically backtrack to somewhere in the neighborhood of 4145 and 4090. The S&P 500 closed on Tuesday, September 26, at 4273, which means the current maximum drawdown is in line with the magnitude of the typical drawdown in the twelve historical cases listed in the table above. The dotted horizontal lines on the chart below allow us to track the typical drawdown versus the current S&P 500 drawdown. Other reference points are shown between 3800 and 4200, including the upward sloping 200-day moving average in red.

It is not unusual for an existing uptrend to backtrack or give back a significant portion of the prior bullish move before resuming the primary trend. The 38.2% retracement of the A to B S&P 500 move shown below comes in near 4180. The 50% retracement sits near 4050. The 61.8% retracement near 3920. Thus, it would not be out of line with typical human behavior if the S&P 500 revisited the 4180 to 3920 range prior to resuming the primary bullish trend. We would learn something about increasing bearish probabilities if the S&P 500 remained below 3920 for an extended period. Wednesday’s close was 4273. The S&P 500’s 200-week moving average currently sits near 3920, which means a typical retracement of 38.2%, 50.0%, or 61.8% would see the S&P 500 remain above or near the 200-week moving average.

The daily S&P 500 chart below shows the much-improved look of the 200/225/250-day moving average stack. The chart also highlights the S&P 500’s range (4200-3800), which represents an area of possible support.

The chart of the NYSE Composite Index below shows price is near the top end of a broad and important band of potential anchored volume weighted average price (AVWAP) support. It would damage the bullish case if the NYSE Composite cannot make a stand above/near the red and light blue AVWAP lines tied to the COVID high and COVID low. Price tested those lines earlier in 2023.

A similar AVWAP chart for the S&P 500 (below) shows price testing an important cluster of possible support.

A zoomed-in version of the same AVWAP chart shows why 4200-4070 represents a key battle region for the bulls and bears. The secular trend thesis would be damaged by an extended stay below the 200-week moving average, which sits near the blue and orange AVWAP lines tied to the COVID high and COVID low. We will learn something about the sustainability of the current bull market based on outcomes between current levels and 3380-ish. We are not making any assumptions about the hold vs. breakdown question. We will see how things unfold in the coming days and weeks.

THE BAD

The VIX looks like it may be trying to get noticed again. The bad news is it was approaching 20 during Tuesday’s session. The good news is “what once acted as support in 2022 and early 2023 may now act as resistance”. Possible resistance in the VIX aligns with possible support in risk assets.

AND THE UGLY

Interest rates have been rising and the Fed’s Neel Kashkari posted the following Tuesday:

Once supply factors have fully recovered, is policy tight enough to complete the job of bringing services inflation back to target? It might not be, in which case we would have to push the federal funds rate higher, potentially meaningfully higher. Today I put a 40 percent probability on this scenario.

Kashkari gives the soft landing scenario 60% odds and the less-friendly scenario 40% odds. The chart of LQD below is also a mixed bag. On the positive side, it has nailed down the same monthly bullish cross that is in play on the chart of the S&P 500.

The bad news is the right side of the base on the daily chart below does not inspire confidence in its present form. The bullish cases for the stock market and economy would take a hit if LQD fails to hold the October 2022 gap, and more importantly, fails to hold above the October low.

SUMMARY

The bears still have control of the short-to-intermediate-term trend. The bulls still control the primary trend. If energy prices, interest rates, and still-elevated inflation push the Fed to hike significantly further than previous expectations, the rally off the October low could fail.

The bears have covered the easy (low support) areas in recent weeks; their task will get much more difficult between 4200 and 3800. On Tuesday, the S&P 500 closed above an upward-sloping 200-day moving average and an upward-sloping 200-week moving average, which makes it easier to see how the now-more-difficult battle unfolds between the bulls and growing-ever-more confident bears.